Treasury yields are rising, stocks are sinking.

And tech stocks, in particular, are getting hammered. It’s a race to the bottom for growth as investors contemplate a larger correction, even after weekly jobless claims came in better than expected this morning.

First-time filings for unemployment totaled 745,000 last week, falling just shy of the 750,000 estimate.

“We’re back to good news (for the economy) is bad news (for the market) and as interest rates move higher on expectations of better economic growth it has been hurting the stock market,” wrote Chris Zaccarelli, chief investment officer at Independent Advisor Alliance, in a note.

All three major indexes are down as of noon.

The Nasdaq Composite, however, seems to be in the most peril. The tech-heavy index broke key support this morning, sinking below 13,000 for the first time since early January. Tech stocks rely on low rates to chase aggressive growth via cheap debt.

When rates spike, tech shares typically drop. And long-term, falling Treasury yields have given tech an edge over the market’s more value-based sectors.

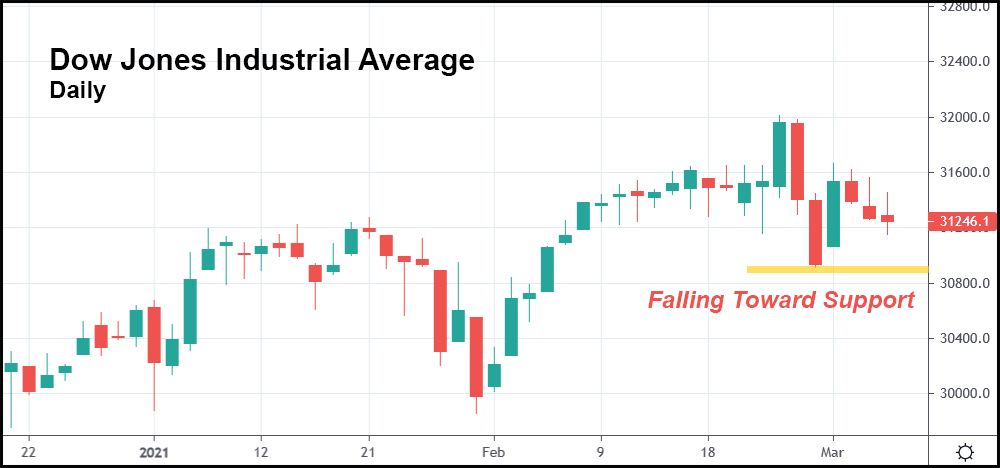

That’s why Dow components have done comparatively much better over the last week, as they’re less wounded by rising yields.

The Dow is down, but it’s not at support just yet. The index will encounter support in just a matter of days if it remains on its current trajectory.

For now, though, it’s fighting to remain in an uptrend. The industrial, energy, and basic material sectors have outperformed the rest of the field.

All while the broader market struggles to stave off a downside breakout.

The S&P is sitting right on top of support, placing it between the Dow and Nasdaq in terms of bearish pressure. That makes sense, of course, as the S&P is made up of both Dow and Nasdaq stocks.

Tech has been dragging down equities since late February. If they continue plunging, which seems likely given the Nasdaq’s dip beneath support, Dow components could eventually get dragged down also.

That would manifest on the S&P 500 chart as the general market sinks into a “nowhere to hide” correction.

Should bulls be scared? In the short-term, absolutely.

But the market’s long-term prospects still skew bullish. The Fed’s not going to let Treasurys go quietly into the night. The White House is intent on providing additional stimulus, too, regardless of how many states completely reopen.

“Our macro team sees the economy as spring-loaded given the vaccinations and additional stimulus,” explained Keith Lerner, Truist chief market strategist, in a note.

“The ability and desire of the consumer to spend on services and experiences should lead to the best economic growth we have seen in over 35 years.”

That begs the question:

Is additional stimulus necessary? It might not be, and it could ultimately contribute to significant economic overheating. But bulls are going to love the next stimulus package nonetheless.

Better yet, quantitative easing – the market’s biggest boon over the years – isn’t going anywhere, either. These bullish forces are likely to keep equities afloat, even if they push inflation to dangerous levels while severely slashing the market’s real gains.

Stocks will eventually puke up their government-given returns, but until they do, the bloated market should continue to mushroom while enduring wild, volatile “hiccups” along the way.

{kind=link}