Stocks jumped this morning in anticipation of a weak inflation reading tomorrow. The Dow, S&P, and Nasdaq Composite all gained, rising strongly through noon. Tech shares led the way while Treasury yields slipped.

It was a nice change of pace following last week’s losses, which were the worst in almost two months. Growing uncertainty over monetary policy had investors ready to sell following the big January rally.

“The market is starting to sense that the very comforting disinflation story is more complex than we’d like it to be,” said Allianz chief economic advisor and noted Fed critic Mohamed El-Erian.

Tomorrow’s Consumer Price Index (CPI) release could make the situation much simpler if it shows that inflation trended lower again. On the other hand, a “hot” reading would only complicate matters further.

“A combination of strong economic data and Fed guidance (January’s jobs report and Powell’s comments last week, mostly) have convinced markets that rates may be ‘higher for longer,'” wrote DataTrek analyst Nicholas Colas in a note.

“This week’s CPI report will be important in terms of giving the market more information on this key issue.”

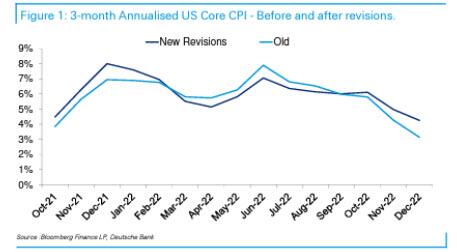

Many traders missed Friday’s CPI revisions, which painted a very different picture of the “disinflation process” – a term that Powell used many times in recent weeks. It was assumed that inflation had cratered in recent months.

Instead, the latest revisions show that core inflation (which the Fed watches more closely than headline) is falling slower than initially reported. Deutsche Bank analysts provided the following chart in a note to clients this morning:

The 3-month annualized core inflation rate is now 4.25% post-revision vs. 3.14% pre-revision. That’s a big difference, and though this is mostly the result of a seasonal adjustment, it makes tomorrow’s data a total crapshoot (relatively speaking) for analysts.

Expenditure weights have shifted, too, and owner’s equivalent rent (OER) will make up a larger portion of the “basket of goods,” rising from 24.3% to 25.4%. This adjustment applies to tomorrow’s release, which means that red-hot rents could result in a surprisingly high core print.

“These revisions, alongside fresh increases in used car prices (Manheim biggest increase for 14 months in January), and the recent strong payrolls print complicates the near-term inflation picture and the job of the Fed,” wrote Deutsche Bank head strategist Jim Reid.

“Some of this uncertainty has been priced in with US 10yr yields up c.+42bps from intra-day lows just 7 business days ago on February 2nd, post what was seen as a dovish FOMC. Terminal rate pricing (July ‘23) has also increased nearly +40bps over the same short period with the December 2023 contract up c.+60bps.”

Reid concluded:

“So, it’s very hard to know what’s priced in for tomorrow market wise, given all the moving parts.”

The market was seemingly able to handle that uncertainty (or investors simply didn’t know about it) as stocks rose strongly today, but buyer beware: these revisions have set traders up for a massive inflation surprise tomorrow.

And, if bulls don’t like what they hear, today’s gains could be gone in a flash due to a seasonal adjustment in basket contributions of all things.

{kind=link}