Stocks showed little change this morning as the market processed incoming “stagflationary” data. The S&P 500 approached its record close of 4,796, with both it and the Dow Jones Industrial Average staying relatively flat, while the Nasdaq Composite ticked up about 0.2%.

Currently, the S&P 500 is on track for its ninth consecutive week of gains, its longest stretch of advances since 2004. Since the start of November, this major average has climbed nearly 13%.

This upward trajectory in stocks over the past two months reflects growing investor confidence that the Federal Reserve might reduce interest rates in March. This sentiment is bolstered by inflation edging closer to the central bank’s 2% target, coupled with the absence of clear indicators of a significant economic slowdown in the U.S.

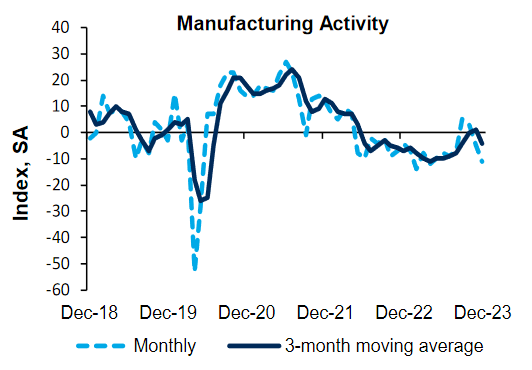

Today’s Richmond Fed Manufacturing Survey, indicating a steeper-than-anticipated decline for the second consecutive month, didn’t seem to rattle traders. The index fell from -5 to -11, a more pronounced drop than the modest -4 that had been predicted.

“Firms remained generally pessimistic about local business conditions, as the index edged

up but remained in negative territory,” read the Richmond Fed’s report.

“The index for future local business conditions was unchanged at -5 in December. Most firms continued to report declining backlogs as the index remained negative.”

This marks a notable shift from the highs seen in April 2022 to the post-COVID lows recorded in December. The survey highlighted declines across all three component indexes: shipments dropped from -8 to -17, new orders from -5 to -14, and employment slightly decreased from 0 to -1.

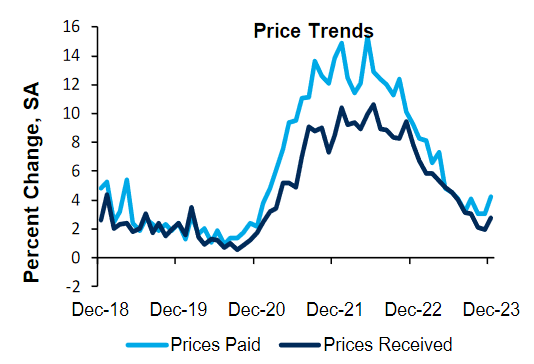

Additionally, both the average growth rates of prices paid and prices received saw an increase in December, with a slight uptick in expected price changes over the next year.

Overall, the survey showed a drop in manufacturing activity (“stagnation”) and a jump in prices (“inflation”), presenting a “stagflationary” reading. And while the Fed is unlikely to be concerned about today’s reading, it may be the start of a trend that ultimately hits stocks at some point next year.

Analysts on Wall Street are wary of this potential outcome, too. Bank of America’s Benjamin Bowler recently warned that it would be one of the market’s top risks for next year.

“With the increasingly strong consensus that the Fed is done hiking, particularly post the October CPI report, an obvious risk would be a surprise re-acceleration or stickiness in inflation that eventually causes the Fed to hike again,” Bowler said.

Don’t forget that the Fed was wrong on inflation in both 2020 and 2021. Fed Chair Powell had to keep the tightening cycle going for much longer than the Fed anticipated as inflation surged. This time around, the Fed will probably be wrong in the opposite direction, having claimed victory too early.

But what about the economy? With key yield spreads now reverting from negative to positive, a recession is assured. There’s over 100 years of market data to suggest that the US won’t escape its recent yield curve inversion (and subsequent reinversion) without one.

Most spreads started to head north again about two months ago. Historically, it’s taken about four months for the US economy to enter a recession after these spreads rise. That means the market is probably going to start seeing serious recession signals sometime in early March, right around when Treasurys are pricing in the Fed’s first rate cut.

If economic activity and earnings wane, though, it won’t be a celebratory cut; the Fed will be cutting purely out of panic. That’s the kind of thing that the market hates and is rarely able to accurately discount ahead of time. There were 15 technical recessions in the US going back to 1933. 81% of the S&P 500’s losses occurred during each recession compared to the 6 months leading up to them, suggesting that the market was unable to see the recession coming.

And that’s the problem; recessions tend to hit when the market thinks there won’t be one. These days, the market really thinks there won’t be one, which will only make the resulting selloff (when it comes) that much worse.

{kind=link}