The market’s closed today in observance of Good Friday, but that doesn’t mean traders have totally taken themselves out of the game. Futures soared this morning after the Bureau of Labor Statistics released the March jobs report, which revealed a massive employment “beat.”

The U.S. added roughly 916,000 jobs last month. It’s far more than analysts expected (660,000) and nearly triple February’s payroll gain of 379,000.

That’s not to say everyone was impressed, though. Bank of America analysts thought 1 million jobs would be added.

Still, it was enough for after-hours bulls who sent all three major indexes higher.

But the biggest winners were small caps, as indicated by the Russell 2000’s 1.27% price surge immediately following the March jobs report. The S&P, Dow, and Nasdaq Composite enjoyed more muted gains by comparison.

It seems “panic buying” is setting in now that investors finally have strong evidence of an economic recovery. In addition, both the dollar and 10-year Treasury yield rose, too, indicating that the market may be pricing in a sooner-than-expected rate hike.

For many months, the “good news is bad news” narrative dominated stocks. When any sort of economic progress was observed, traders took it as a sign that the Fed would taper its bond-buying programs, thus causing yields to rise while harming equities.

Now, though, the dollar, yields, and stocks are all climbing in response to a stunning jobs report. Is the “curse” broken?

It certainly appears that way with today’s futures activity. However, let’s not declare an end to the insanity prematurely. The market has yet to open on Monday. We’ll see what traders really think about the March jobs gain by the end of next week once they’ve had some time to digest it.

More importantly, Wall Street may start to shift its focus to inflation. Last month’s manufacturing report – released yesterday by the Institute for Supply Management – also showed far better than expected data. U.S. factory activity jumped to 64.7, hitting its highest level since 1983.

March’s spike in manufacturing drew concern from inflation-wary economists. Now, they have a massive jobs beat to worry about as well. That’s in addition to last Wednesday’s March Consumer Confidence reading, which measured at a 12-month high.

Nearly every indicator is pointing up in a record-setting fashion. And though this is to be expected during an economic recovery, it’s also the kind of activity that often precedes a “tamping down” by the Fed.

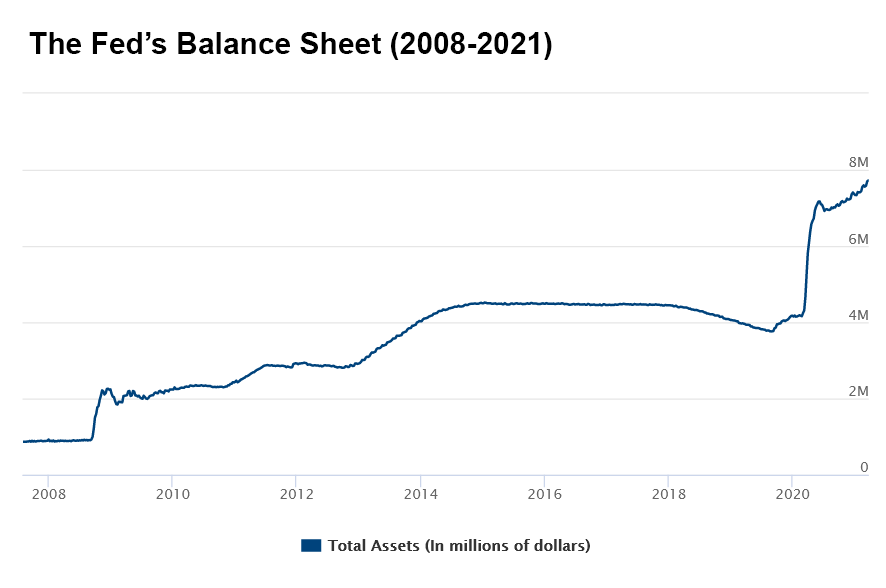

Except, in this case, Fed Chairman Jerome Powell said that rates wouldn’t move until at least 2023. He claims to be watching inflation in regard to altering rates, but in reality, he’s got far bigger fish to fry. After 12 years of quantitative easing (QE) and a pandemic-driven doubling of the Fed’s balance sheet, Powell can’t raise rates without causing massive damage to nearly every market.

To Powell’s credit, he attempted to induce quantitative tightening back in 2018 by unloading Treasurys and raising the federal funds rate. That caused a dip in the Fed’s balance sheet and a wicket correction in the stock market.

It was a noble endeavor, but ultimately something the market couldn’t stomach. And that was at the height of an economic boom with record-low unemployment when the Fed “only” held $4 trillion in securities.

Imagine what would happen if the Fed raised rates next year and attempted to reduce its nearly $8 trillion balance sheet. Do you think it would go smoothly?

Or, would it possibly resemble 2018’s bearish reaction instead?

My bet would be on the latter. It’s long been assumed by skeptical economists that QE is a “roach motel.” Once your economy checks in, it can never check out.

Powell’s rate hike gambit in 2018 likely proved that to be an accurate assessment. And if the Fed tries it again, a repeat performance is likely to follow.

Except this time, the roaches (or investors) could get squished with far greater ferocity as they rush to find an exit, only to hit a “brick wall” of panic selling on the way out.

{kind=link}